Comments On SEC Proposal for Semiannual Reporting

News Analysis & CE for Investment Advisers

| CE Status | ||

|---|---|---|

| Organization | Status | Course ID |

| NASAA | Approved | C82188 |

| IWI | Approved | 26A4AI30285 |

| NASBA | Approved | |

| CFP Board | Approved | 350522 |

Fiduciaries and semiannual reporting collide at the point where a portfolio holding no longer supplies the same regular 10-Q evidence.

Last updated July 1, 2026

What happens when the world’s largest capital market reduces the required frequency of standardized public financial information?

We may soon find out.

The SEC has proposed a rule allowing public companies to stop filing 10-Qs and file semiannually financials instead.

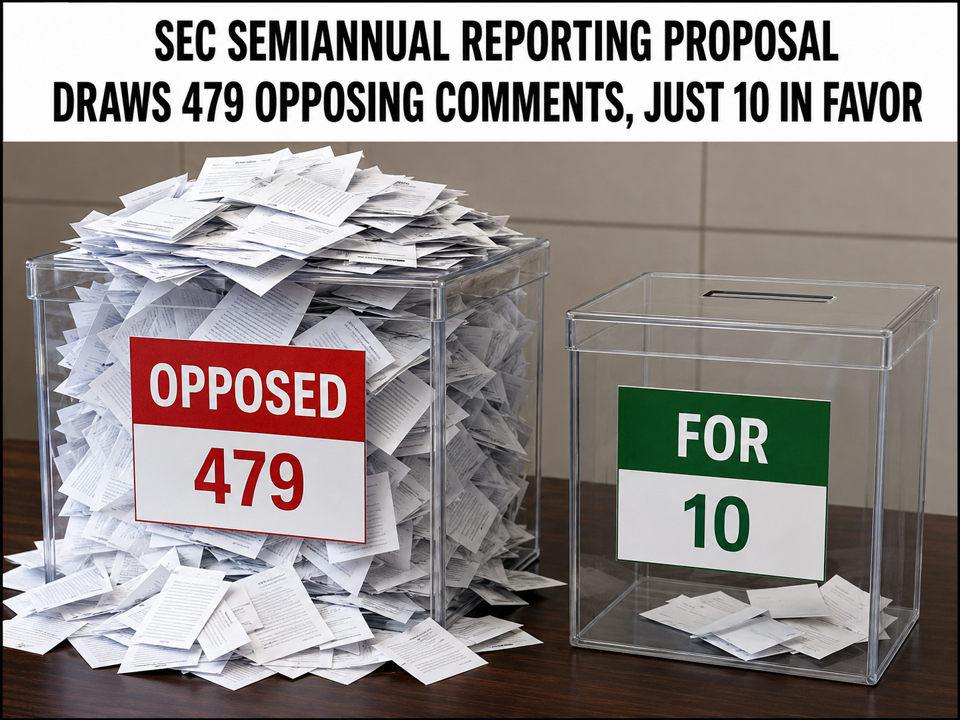

A major finding of the compilation and analysis of the public comments: the SEC proposal for semiannual reporting is drawing overwhelming opposition.

The analysis reviewed 511 records, including 507 public comment letters and 4 SEC meeting memoranda. Of the public comments, 479 opposed the shift or urged the SEC to keep quarterly reporting, while only 10 were counted as strictly pro-semiannual and 9 were mixed or conditional.

Commenters were roughly 98% opposed and 2% in favor of semiannual reporting by publicly held companies.

Commenters viewed the proposal as a change in the cadence of formal standardized public information and not merely a recordkeeping change.

Opposition came from retail investors, advisers or financial professionals, and investment club members.

At this class, investment advisers learn how to:

Explain the 479-to-10 response, the SEC's public comment process, and deadline. |

Describe how Form 10-S changes interim reporting cadence. |

Explain why adviser duties don't change despite fewer filings and disclosures. |

View commenters as investor proxies in analyzing their responses. |

Distinguish SEC forms, earnings releases, and guidance. |

Evaluate accounting-profession concerns about audits and interim reviews. |

Analyze retail, professional, institutional, and investment-club commenters. |

Assess fiduciary monitoring risks and accounting integrity concerns. |

Evaluate issuer-flexibility arguments and market-risk concerns. |

Apply historical context and communicate practical client responses. |

At least 300 comments mentioned one of these investor types, and at least 160 identified as retail, individual, private, personal, retirement, or self-directed investors, 42 involved financial or capital-markets credentials, and 16 referenced investment clubs—Better Investing, NAIC, or similar groups.

Another key finding of the analysis of the comments is the change the proposed rule's adoption would make to fiduciary risk. If companies elect semiannual reporting, advisers still must monitor holdings, explain recommendations, and document a prudent process, even if they have less regular form 10-Q evidence.

Pass a 10-question quiz by scorug at least 70% and complete three ungraded review questions.

IARs, CFP® , CIMA, CPA, CPA/PFS professionals as well as CFAs.

Free to Advisors4Advisors members ($60/quarter) or $29.99 for non-members

Credit Hours: 1

Field of Study: Ethics

Course Level: Intermediate

None

None

Reading a 9750-word document optimized for CE (DOCE®)