Our Observations On The Economy: We Expect Inflation, More Foreclosures, And A Continued Rise Of China's Economic Power

Unfortunately, due to the income tax bill passed in December, which in effect results in an income tax freeze for 2011 and 2012, the budget deficit appears to be on pace for similar deficits as occurred in the last two years.

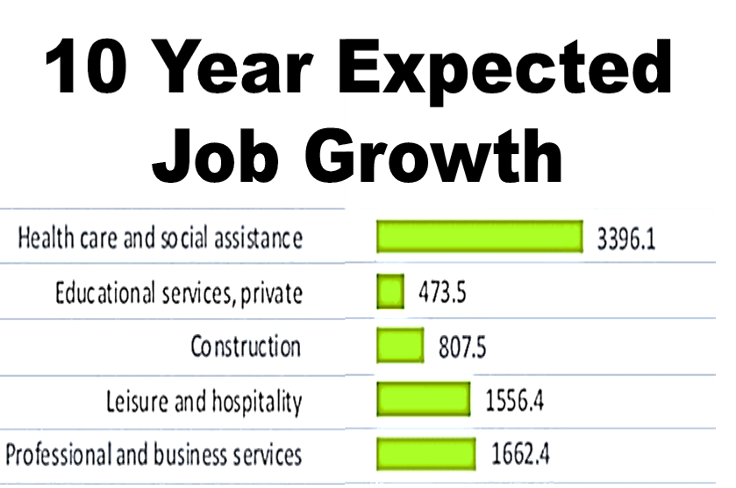

On the surface, the U.S. economy continues to improve ever so slowly, showing more of a limp “L” type recovery versus the usual “V."

Given the pathetic rate of improvement in some areas, especially unemployment and housing, that we’ve made over the past two years, it certainly does not seem to warrant that amount of spending. However, when looking below the surface, so to speak, it is likely we would be in a Depression--but not a Great Depression--were it not for the mammoth amount of Government spending since the Fall of 2008.

In fact, to find a similar economic period in history, given the debt problems we currently have, you'd have to go back to the 1906 to 1914 period--although the debt this time as a percentage of Gross Domestic Product (GDP) is far larger this time (approximately 370.0% versus 260.0%). During that nine-year period, there was a recession as well as three of what was then called depressions or panics.

Notice we qualified that statement, although they may have actually been deep recessions. As a side note, recessions result in a decrease in GDP of 0% to 5.0%. What is often termed by the media as “The Great Recession” was actually a recession. A severe recession is a decrease in GDP of 5.0% to 10.0%, and a depression is defined as a decrease in GDP of 10.0% to 25.0%. A Great Depression is defined as a decrease in GDP of 25.0% or more.

It's difficult to determine the severity of the economic downturn of the early 1900s due to the fact that economic data was either not kept, or was not available to the degree it is today. However, we eventually emerged from that dire economic period due to the positive economic performance that was generated from World War I.

At some point, consequently, we expect the U.S. Government will effectively give up and then reflate the economy. Inflation makes GDP larger while debt does not inflate, thereby, making the debt amount smaller as a percentage of GDP. That can bring down our debt to a manageable level relative to the size of our economy. In order to accomplish this feat, we will need high single-digit inflation to occur for at least 10 to 12 years or a higher inflation rate over a shorter time period.

The Alt A and Option ARM mortgage problems peaked in late 2009, and mortgage defaults would normally occur six to nine months later. Well, to some degree we’ve arrived. To “some degree” means because the delinquencies (90 days or more overdue) have occurred at a rate of 13.0%, yet foreclosures are far behind that level at approximately 5.0%.

Banks have, until this point, been reluctant to foreclose on homeowners for several reasons. Among them, the Government and the banks would like to avoid that scenario as much as possible due to the concerns about first, bank capital—when a bank forecloses on a home, the bank has to write down the mortgage to its true value, thereby, eating away at bank capital and perhaps jeopardizing the bank’s viability to continue its operations. Therefore, the banks often won’t foreclose—a banking strategy now known as extend and pretend. If the loan is not foreclosed upon the mortgage/home does not have to be written down. In effect, the bank pretends that it owns a fully amortizing mortgage.

The U.S. Government itself, of course, doesn’t want banks to foreclose due to the fact that the banking system could end up in jeopardy. Yet in calendar year 2010 there were approximately 2,900,000 foreclosure filings issued after 2,600,000 plus in 2009 were issued.

To help minimize the impact delinquent home mortgage borrowers might have on the banking system, the Government’s Housing Affordability Mortgage Program (HAMP), which provides borrowers with the opportunity to modify the terms of the mortgage with regard to the principal and interest payments (and stay in their homes); in other words the Government subsidizes payments.

- Poorer capitalized banks.

- Many homeowners with significantly lower credit ratings.

- Even lower housing prices nationwide.

- Increased Inventories of homes now over 3,000,000 [excluding what is called the shadow inventory (mortgages that are in or nearly in foreclosure but are not yet on the market) and getting worse] which causes new home construction to be depressed.

- More people will lose their homes.

Unfortunately, due to our debt load, little economic issues become big ones. In the long run the total debt, which is approximately 370.0% of Gross Domestic Product (GDP) has to decrease.

If you don’t believe this, look at the Chinese. They have over $2.6 trillion in reserves, and it now appears that the Chinese make the economic rules and everyone else tries to get out of their way or work around them. After all, isn’t our government continually asking the Chinese to increase their currency value against the U.S. Dollar to minimize the Chinese imports to us and maximize our exports to them. Who is begging who?

This Website Is For Financial Professionals Only