Stress Testing: The Coming Paradigm Shift

I. Stress Testing - Macro Scenarios

To effectively understand stress testing we need to look at macro risk scenarios like Obamacare, the end of QE, and many others. The events of the Great Recession have left the public deflated, skeptical, and clutching their dollars. Macro risk, especially policy risk, is here to stay as a major influence on any portfolio and a vocal concern of clients. Anticipating macro risks, taking hedged positions to counter downsides, and aptly answering client concerns are key to minimizing risk exposure and improving bottom lines for advisors. Fortunately, there is technology that can be leveraged to give even single-advisor offices the same edge a wirehouse has.

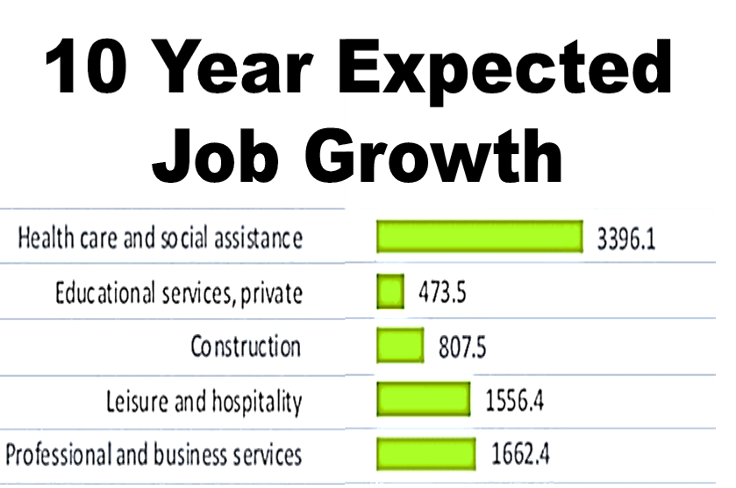

HiddenLevers is a software provider with a stress testing toolkit of over 60 customizable scenarios to stress test out of the box. These comprise of historical, forward-looking, and Federal Reserve scenarios. Here, we see the Fed's adverse scenario, represented as movements in the primary economic levers.

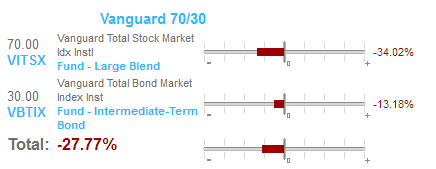

And the corresponding impact this scenario has on a typical 70/30 portfolio:

First, the 70% equity position closely tracks the market. The bonds mitigated some of the loss and this portfolio was down almost 28% instead of the market’s 34%. If a client comes in with a simple allocation split like this, then there’s the beginning of a conversation for better investment strategy based on data. This sort of real exchange will go further in motivating action and fulfilling fiduciary duty. The other option - ignoring macro risk - leaves fiduciary duties unfulfilled.

In a bull market, stress testing can help locate the right vehicle to take advantage of positive economic trends, like a housing rebound. In the Fed’s baseline scenario, with the market up 10%, advisors need to ensure their equity positions, at a minimum, track the market. Stress testing can be used to see how much of that growth is captured. This is accomplished by determining an investment vehicle’s correlation with trending indicators.

II. Stress Testing – A Fiduciary Duty

The Dodd-Frank Act mandated banks begin stress testing their holdings, and the Fed implemented this with scenario-based stress tests simulating baseline, adverse, and severely adverse market environments. International regulations (Basel III) now require stress testing at all major global banks (See: Part 1, Paragraph 21 - http://bit.ly/1e1VwjY ). With financial institutions assessing the risk parity of the market, advisors should also consider stress testing portfolios. This complements both verifying risk tolerances and fulfilling fiduciary duty.

Clients can rarely grasp the reality of an index’s shift during a market correction. According to an InvestmentNews article from December, 98% of U.S. equity fund inflows in 2013 went to Vanguard Group Inc. That’s $41.4 billion dollars (See: http://bit.ly/1g8kBx3 ). If this doesn’t compel advisors to differentiate themselves and add value, then I don’t know what will. The argument that riding the index over a long period of time will mute any volatility and provide returns without high fees has found an audience. And it’s 98% of the money.

However, we know from behavioral economics that losing one dollar is three times as painful as gaining a dollar. Riding the index still makes the stomach lurch with every correction. More importantly, many clients five years away from retirement don’t realize they’re in the most critical period for their portfolio. A market drop in this pre-retirement window is almost impossible to recover from and can diminish one’s quality of life permanently; this occurred too often during the Great Recession. The near-retirement population may have the greatest need for stress testing from a fiduciary standpoint. They’re most at risk to the repercussions of a market downturn. A 20% market correction occurs every 4 years. A 10% correction happens every 18 months (See: http://bit.ly/1dASYER ). Stress testing can help identify these risks so advisors can take action.

III. Stress Testing - The Need for a Tech Solution

A paradigm shift is coming. Most advisors want to be proactive and forward thinking, it’s necessary for long-term success. Dodd-Frank and Basel III have changed the national and international banking system. Ultimately, this same scenario-based stress testing done at the bank level will be part of the fiduciary duty of financial advisors and planners. There is a gap between what is expected of fiduciaries and what they are capable of as non-quants. HiddenLevers founders asked the age old question - Can a tech solution bridge this gap? Four years later, we have a technology toolkit that is both effective and easy to use, to make portfolio stress testing a reality for financial advisors everywhere.

Tech Development Benchmarks

|

Effective |

Easy to Use |

|

· Automate the regression modeling done by the quants at big banks. · Create a library of possible macro events, including the Fed stress tests. · Make the stress testing results client friendly and easily digestible. |

· Have a cloud-based solution accessible from anywhere and on any platform. · Make it pretty and interactive so it has built-in marketing. · Create alerts and a portfolio monitoring system so advisors can focus on what matters. |

IV. Stress Testing - Everybody’s Doin’ it

Although stress testing is a new focus of the Federal Reserve, private Wall Street banks, Black Rock, and other high-end institutions have been stress testing holdings for years. It used to take a dozen quants crunching equations in excel sheets to produce results. They laid the groundwork for what can now be done automatically, thanks to the growth of technology. It’s only recently that this analysis has been made available to advisors and in a client-friendly way.

Other risk monitoring tools like Monte Carlo simulations and VAR have been around for a longer time, but haven’t held muster in events like the Great Recession. Unfortunately, Monte Carlo simulations are not designed to model the rarer tail risk that can detriment a pre-retirement portfolio. Stress testing is how fiduciaries account for tail risk, make downside risk resonate with clients, and map potential upside opportunities. Macro impacts are how clients see the world and how the markets are behaving.

That’s right. The ups and downs of the market demand stress testing. High-end firms have been doing it for years, the Federal Reserve now has banks doing it. Stress testing may soon become an integral aspect of fiduciary duty. Be ahead of the curve, not behind it.

######

By Joonas Niiholm, HiddenLevers

This Website Is For Financial Professionals Only