U.S. Could Become Energy Exporter By 2030: Glut of Cheap U.S. Gas From Shale Rock Offers Plenty Of Investment Opportunities

Main Conclusions

The BII report offered the following conclusions in its report:

- U.S. oil production is growing thanks to the boom in shale oil— reversing a decline since the early 1970s. Getting the oil to market, however, is a huge challenge. Keeping close tabs on this conundrum can help investors identify opportunities in energy infrastructure. It also gives insights into future price differences between global and U.S. oil prices.

- Shale reserves abound around the world, with vast deposits in countries such as China, Argentina and Poland. But the scale and speed of the U.S. boom is unique, and cannot be easily replicated elsewhere. Reasons include well-documented and cooperating geology, an experienced and competitive exploration industry, and well-established ownership and property rights.

- Most energy analysts project a global energy supply gap caused by depletion of traditional oil fields and steady demand. U.S. shale exploration is unlikely to close this gap. In fact, traditional OPEC members are likely to expand their share of world capacity, according to research firm Wood Mackenzie. One big caveat is many energy supply projections assume robust global growth of around 3%—a pretty hefty rate in today’s climate.

- The U.S. is awash in gas, helping knock down U.S. prices to record lows—and below many producers’ costs of production. U.S. gas reserves are generally estimated to be ample enough to last a century. Improved drilling techniques could significantly extend this time frame. This raises the prospect of U.S. energy self-sufficiency and may be a boon for energy-intensive industries such as chemicals and heavy manufacturing.

- The great U.S. gas glut is here to stay. Gas prices in Asia are about seven times higher than in the U.S., but there is no easy arbitrage yet. Exports require huge investment in liquefying gas and transporting it to market. Companies are slashing capital spending and pulling gas rigs, but we do not yet see a real hit to production and a quick rebound in prices.

- Deal activity and other indicators (including a 1,000% rise in the price of Indian guar beans used in the process of extracting shale oil and gas) show the boom’s intensity. The BII expects more takeovers in the fragmented industry as many producers are hungry for cash and some risk violating their debt covenants.

- Private equity funds would be likely buyers because they can afford to take the long view on gas prices.

- Gas and alternative energy such as wind and solar power will likely replace coal and—to a lesser extent—nuclear energy as top sources of electricity generation in the developed world over the next two decades. BII does not believe cheap gas spells the end of alternative energy. Alternatives are starting to compete on price—even without tax incentives in some markets.

- Some wind farm operators have locked into long-term supply contracts with utilities, still a rarity for gas producers.

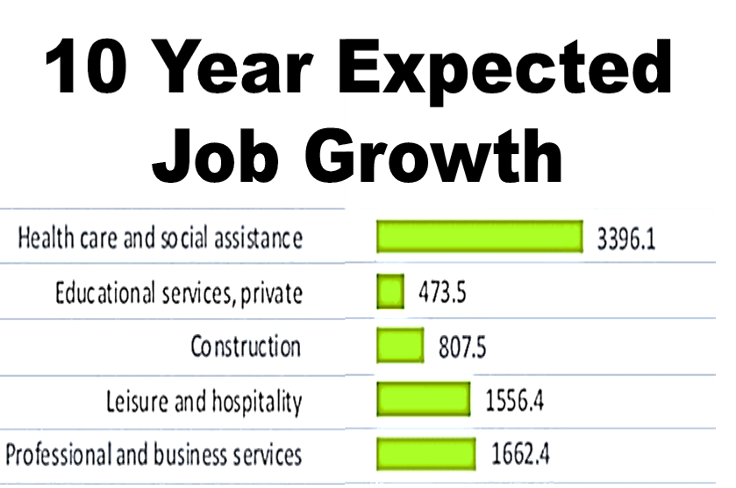

- Politics and public opinion matter. The process of fracturing rock to extract oil and gas from shale has come under fire by environmentalists. They worry about chemical spills, a depleting water supply and the risk of causing (minor) earthquakes. They are pitted against shale industry proponents highlighting job growth and energy security.

So What Are The Investment Opportunities?

According to the BII, there are several ways to take advantage of current trends in energy world.

- Infrastructure: The BII favor companies that facilitate the transport of energy, such as pipeline operators and those that benefit from investment in building out the U.S. energy infrastructure.

- Services: BII likes like oil service companies specializing in deepwater exploration—the area where major oil firms are directing a quarter of their investments. The BII also like service companies with international operations as beneficiaries of growth in emerging markets.

- Exploration: The BII is focused on exploration companies that could benefit from a rebound in gas prices, U.S. shale growth, the resumption of Gulf of Mexico drilling, and East and West Africa exploration

- Oil and Gas Prices: The BII presently favors oil over gas and oil explorers over gas producers. Among the reasons why, the BII says U.S. natural gas prices should rebound in the medium term, but it is tough to see a catalyst for a big reversal in 2012.

- Alternatives: Developers and operators of wind and solar farms are attractive. Avoid manufacturers because of intense competition. BII says it’s closely following start-ups experimenting with new technologies such as low-energy nuclear reaction and fusion. BII says investors should follow developments in new technologies closely, but will treat them as side bets until they reach economic scale.

- Coal: Coal prices and producers have been beaten down so much that they may be in for a reversal. Within the sector, the BII focuses on producers of metallurgical coke, used in smelting iron and blast furnaces.

- Utilities: U.S. utilities, long a favorite of investors focused on steady earnings and high dividends, are likely to become more volatile as energy prices fluctuate.

- Guar: And finally, the BII says Guar prices look rich. BII is happy for the Indian farmers growing the beans, but investors tempted to buy at these levels should tread carefully. Whoever develops a synthetic alternative to guar gum deserves a thorough look.

Of note, the Wall Street Journal in a front-page story today notes that “America will halve its reliance on Middle East oil by the end of this decade and could end it completely by 2035 due to declining demand and the rapid growth of new petroleum sources in the Western Hemisphere.”

According to the WSJ report, “the shift, a result of technological advances that are unlocking new sources of oil in shale-rock formations, oil sands and deep beneath the ocean floor, carries profound consequences for the U.S. economy and energy security. A good portion of this surprising bounty comes from the widespread use of hydraulic fracturing, or fracking, a technique perfected during the last decade in U.S. fields previously deemed not worth tampering with.”

And in a separate but related report, the U.S. Energy Information Administration says U.S. demand for energy will increase less than 1% annually through 2035, and reliance on imported oil will steadily fade. During the next decade, imports of crude oil will decrease 2 million barrels daily, cutting spending on foreign oil by $58 billion annually at existing prices, the agency said according to this CBS MoneyWatch/The Associated Press report.

This Website Is For Financial Professionals Only